showCASE no. 94 I The Warsaw Stock Exchange: As Goes the Stock Market, so Goes the Whole Economy

The Warsaw Stock Exchange in brief

With a current head count of 50 foreign companies and total capitalisation (as of 7 June 2019) of PLN 1,128,595.70 million, the Warsaw Stock Exchange (WSE) may now be one of the largest and most developed equity markets in Central and Eastern Europe, according to FTSE. How has that come to be?

Although first attempts at reviving capital markets in Poland were tentatively undertaken after the end of the WW2 in 1945, the idea of a stock or commodities markets was ideologically forbidden under the centrally planned economy of post-war Poland. It was not until thirty years ago – in September 1989 – that the newly formed non-communist government started a series of reforms aiming at the (re)introduction of the market economy. These efforts were fuelled by privatisation processes and development of equity markets occurring in parallel.

While similar processes in other economies may have been conducted via existing legal and market structures, arising organically with the demands of the market, Poland had no such institutional structure. A break of more than 50 years in the functioning of the national equity market created a gaping void which had to be filled with new institutional imperatives and legal arrangements fit for the modern market economy. However, the newly drafted legal solutions did not address sufficiently the issues related to functioning of a country’s financial market. Thus, the country’s authorities reverted to the pre-war commercial code (based on a Presidential Decree of 1934) to define the rules applicable to, for example, public joint stock companies. Still, the modern WSE was not solely based on Polish tradition. In light of the growing globalisation trends, it was decided to use an international model of stock market. This option allowed for a dynamic development and internationalisation of the market. The latter process started at the very beginning of the design of the stock market; while much work had been undertaken by Polish experts, it was Société de Bourses Françaises which provided financial support and expert knowledge, together with Central Securities Deposit SICOVAM (the WSE was modelled on the Lyonnaise stock market). This external support, while not devaluing national ideas and pre-war solutions, such as the commercial code (which, despite dating back to 1934 was the only ready legal act at hand) appeared to provide greater chances for success.

Putting in place an appropriate legal framework to accompany the Polish-French emerging creation was vital: in 1991 the Parliament passed a bill regulating the functioning of the financial markets’ most important players. As for the stock exchange itself, the bill stated that this institution should aim to balance supply and demand, enable market valuation, preserve transactional security, and disseminate uniform information allowing investors to assess the current market value of traded securities. On the 12th of April 1991 the WSE’s founding act was signed; four days later the very first session – participated by five companies and seven brokerage houses – took place. Indeed, in the first decade of the WSE’s functioning, the pre-war solutions combined with the French expertise may have seemed sufficient – only in the early days of the 21st century did the legislative works commence to replace the outdated commercial code.

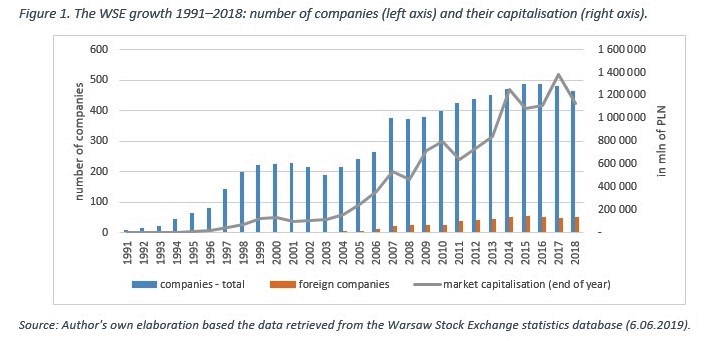

Since that day, the WSE has been growing at a rapid pace – just ten years from its commencement there were 230 firms active on the market, with the stock market capitalisation reaching an end-of-year level of ca. PLN 103,370 million, an impressive increase of 641 times its original level. However, 2001 saw relative drop in the market worth of companies; the following years saw a steady and persistent growth with few – in perspective, relatively inconsequential – dips.

In 2004, Poland not only acceded to the EU, but it hit another milestone as the first foreign companies started to appear on the Polish equity market. Over the last fifteen years, their numbers have been steadier than the domestic firms. Currently there are 461 companies traded in total, with 50 foreign companies accounting for nearly 50% of the total capitalisation.

As goes the stock market, so goes the whole economy?

The importance – and role – of the stock market in economic development has been widely debated in empirical and theoretical literature. Equity markets are thought to approximate the moods of investors in a given country and its state of economic well-being. First efforts at identification of these relationships date to the inter-war period, and since that time financial markets have been an acknowledged driver of economic growth at many levels.

In general, stock markets employ capital (which would otherwise rest idle as savings) to lucrative activities. Yet, the real economy also influences the development of the stock markets: it provides surpluses which feed into the financial sphere. While the existence of this mechanism complicates scientific studies and fuels multi-directional and interdisciplinary research, it has also its more tangible effects in form of policy formulation. For example, assuming that causality between financial markets and economic growth was unidirectional, it has been recommended that any obstacles to growth, including regulatory frameworks, should be eliminated so that shareholders’ welfare (wealth) becomes priority.

This recommendation notwithstanding, the economic effects of stock market growth – measured by liquidity, among others – facilitate investments by allowing trade in equity and debt securities without forcing investors to freeze their means. On the flip side, long-term economic growth might be negatively affected: higher returns on the stock market are likely to attract more investors (and investment) and, perversely, decrease the rate of savings in an economy as investors could consume a greater share of their incomes and replace future consumption with the current consumption, hampering capital accumulation. Additionally, investing in highly liquid financial markets is less risky: while investment is thus more attractive, precautionary savings[1] decisions are not, which creates a dynamic of a dubious impact on the economy. Lastly, one may argue that a very liquid equity market and a near-frictionless trade in securities contributes to investors’ myopic decisions which could filter to corporate policies in the area of financial governance, thus reducing demand for accountability.

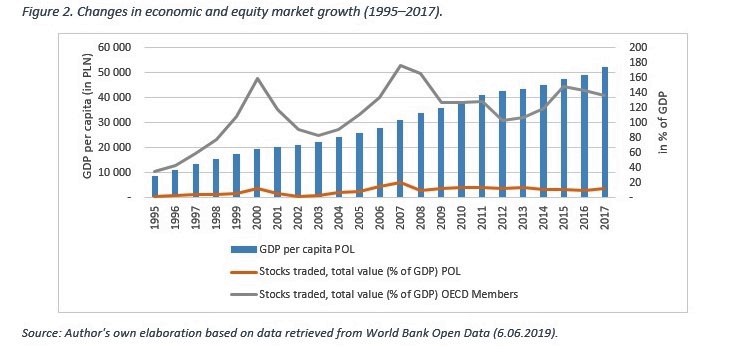

Scientific debates do not always find their reflection in reality. Taking the afore-mentioned market liquidity as an example, we observe little connection between it and economic welfare in Poland (measured as GDP per capita) over the past two decades (see: Figure 2). Indeed, while the latter increased steadily, the WSE’s liquidity had difficulties in staying over 20% of GDP (in fact, this feat was achieved only in 2007), consistently oscillating between 7% and 12% of GDP. In terms of growth, between 1995 and 2017, Polish GDP per capita increased nearly six-fold, while the stock market liquidity lagged behind (for example, as compared to the OECD average).

Yet, numbers can be misleading: in September 2018 Poland emerged as the first post-Soviet bloc country which was deemed worthy of “developed economy” status by FTSE. Earning the status demands meeting all 21 Quality of Markets criteria related to such areas as market and regulatory environment, functioning of derivatives, and dealing infrastructure, among others.

In line with the FTSE’s stance, Polish equity market regulatory authorities have managed to maintain a sufficiently investor-friendly, international environment together with minority stakeholders’ protection and contract enforcement. In addition, apart from being open to inflows of foreign capital, the Polish economy has also managed to maintain the World Bank criteria for “high-income” economies.

Moving forward, (not) looking back?

Being upgraded to the “developed markets” group and thus placed next to financial markets of Germany, France, and the UK (for example) comes with a catch. Some might argue that achieving such a status might be easier than sustaining it. Developed markets are required to maintain an open capital market, allowing foreign investors unrestricted access to local securities and the right to repatriate their assets at will without much administrative impediment. Opening of financial markets has further costs, including imposing policy discipline as far as fiscal and monetary solutions are concerned. Despite governmental pledges and reform plans aiming to strengthen the domestic financial market and invite investment, the price of failure is very high, as exemplified by destabilising effects of capital flight. On the flip side, if the country maintains this status, the gains to be reaped are substantial: beginning with cheaper investment financing via overseas savings rather than being forced to rely on domestic (pricey) capital and obtaining additional sources of risk diversification.

Poland – the EU’s eighth-largest economy – despite its continued struggle to be considered as a developed economy, has been criticised in the past for not doing enough to propel development of its financial markets. When it was first classified by the FTSE in 2004, Poland failed four out of the 21 QM criteria: it lacked free and smoothly functioning foreign exchange and derivative markets, and the rights of financial intermediaries in international investment were questionable. Fifteen years later, with little institutional memory, the WSE successfully operates several markets – the (main) market for stocks in parallel with NewConnect, an alternative market for up-and-coming firms, derivatives, and corporate and municipal debt securities traded on Catalyst. With more ups than downs throughout its (short) history, the WSE comes across victorious, as an important propeller of Poland’s economic growth and an attractive market for foreign capital.

[1] Saving in this case meaning postponing any future consumption in light of the uncertain future.

By: Anna Malinowska, CASE Economist